U.S. oil market has crashed. The price of U.S. oil turned negative for the first time in history. The U.S. oil industry is facing a doomsday scenario. Hundreds of U.S. oil companies could go bankrupt. Many U.S. oil companies took on too much debt during the good times. Some of them will not be able to survive this historic downturn.

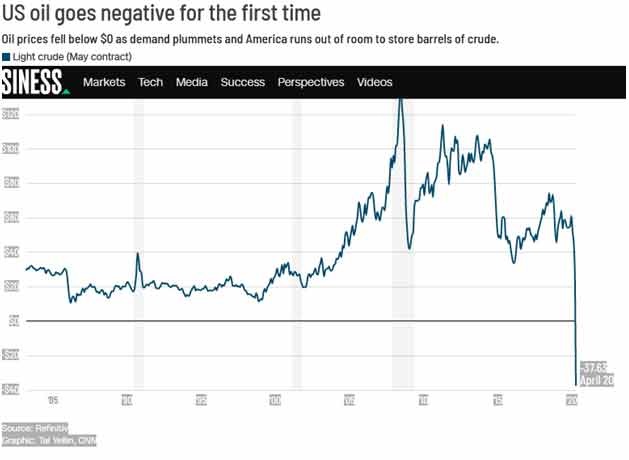

West Texas Intermediate oil prices have gone negative in a record low for the U.S. benchmark, as the market continues to crater amid the general economic collapse.

The price of U.S. oil turned negative means oil producers are paying buyers to take the commodity off their hands over fears that storage capacity could run out in May.

Vanishing demand and a glut of supply have combined to heavily impact the U.S. benchmark fuel, with oil prices dropping from $18.27 to close at -$37.63 a barrel on Monday – down over 300 percent from the previous day’s close. It is the first time the crude oil futures contract has ever traded in the negative since the New York Mercantile Exchange started trading it in 1983.

The collapse in oil markets comes amid a generalized economic downturn, with the coronavirus pandemic plunging most of the world’s economies into a downward spiral many believe will be the deepest since the Great Depression of the 1930s.

The U.S. Department of Energy is nevertheless weighing the idea of paying domestic producers to simply leave the oil in the ground so as not to further depress prices.

With May’s futures contracts set to expire on Tuesday, investors are scrambling to unload their positions, eyeing the already-glutted market and concerned about being left with a valueless commodity.

As the futures contracts hovered at record lows, oil tankers are reportedly languishing at sea, unable to find places to store their bounty onshore. Demand for the commodity has dropped an estimated 30 percent worldwide amid the coronavirus crisis.

The coronavirus pandemic has caused oil demand to drop so rapidly that the world is running out of room to store barrels. At the same time, Russia and Saudi Arabia flooded the world with excess supply.

That double black swan has caused oil prices to collapse to levels that make it impossible for U.S. shale oil companies to make money.

U.S. crude for May delivery turned negative on Monday – something that has never happened since NYMEX oil futures began trading in 1983. It was easily the oil market’s worst day on record.

US crude for June delivery is still trading above $20 a barrel — but even that is disastrous.

“$30 is already quite bad, but once you get to $20 or even $10, it’s a complete nightmare,” said Artem Abramov, head of shale research at Rystad Energy.

Bankruptcy

In a $20 oil environment, 533 US oil exploration and production companies will file for bankruptcy by the end of 2021, according to Rystad Energy. At $10, there would be more than 1,100 bankruptcies, Rystad estimates.

Noble Energy, Halliburton, Marathon Oil and Occidental have all lost more than two-thirds of their value. Even Dow member ExxonMobil is down 38%.

Whiting Petroleum became the first domino to fall when the former shale star filed for Chapter 11 protection on April 2. But it certainly will not be the last.

“At $10, almost every US E&P company that has debt will have to file Chapter 11 or consider strategic opportunities,” Abramov said.

The most stunning part of the record low in oil prices is that it comes after Russia and Saudi Arabia agreed to end their epic price war after U.S. President Donald Trump intervened. OPEC+ agreed to cut oil production by a record amount.

Trump said the OPEC+ agreement would save countless jobs and much-needed stability to the oil patch.

“This will save hundreds of thousands of energy jobs in the United States,” Trump tweeted on April 12. “I would like to thank and congratulate President Putin of Russia and King Salman of Saudi Arabia.”

Yet crude has kept crashing, in part because those production cuts do not kick in until May. Demand continues to vanish because jets, cars and factories are sidelined by the coronavirus pandemic.

The hope in the oil industry is that Monday’s negative prices are somewhat of a fluke caused by the rolling over futures contracts.

The key will be how long oil prices stay dirt cheap. A rapid rebound in prices could allow many oil companies to avoid bankruptcy.

Buddy Clark, co-chair of the energy practice at Houston law firm Haynes and Boone, said his firm is “extremely busy” working on potential oil bankruptcies. Haynes and Boone has been forced to pull lawyers from other areas of the firm to work on the oil problem.

“I don’t think I’ve seen anything like it in my lifetime. It’s unprecedented,” said Clark, who started working in the industry in 1982.

Clark thinks that despite the further collapse in prices, there will still be only — “only” — 100 oil bankruptcies in 2020.

“It’s hard to believe that 100 bankruptcies is the optimistic view. That just shows you where we are,” Clark said.

There would probably be more bankruptcies already if it were not for the extreme volatility in oil prices. Clark said companies are having trouble drawing up restructuring plans because they do not know what the price of the commodity will be.

“Ironically, the lower price has slowed down the process,” Clark said. “A number of companies may have teed up filings but they need to go back to the drawing board.”

The dire outlook in the oil industry will make it very difficult for companies attempting to reorganize in Chapter 11 proceedings to get the required financing and support. Debtholders who would normally swap their debt for equity may not want that equity.

That means, unlike the 2014-2016 crash, some oil companies may not survive altogether.

“Chapter 11 requires financial sponsors to back you. You may see more Chapter 7 liquidations,” said Reid Morrison, US energy leader at PwC.

The nightmare scenario could present lucrative buying opportunities for the industry’s biggest players. That is because struggling oil companies, either in bankruptcy or before it, will be forced to sell off prime acreage — at fire sale prices. Exxon and Chevron, the industry’s supermajors, could be tempted to make acquisitions.

“Those with strong balance sheets will be able to take advantage of the situation,” said Morrison.

However, he noted the supermajors will be “cautious about pulling the trigger” in the next six months because they must defend their coveted dividends first.

Negative territory

Demand for oil has all but dried up as lockdowns across the world have kept people inside. As a result, oil firms have resorted to renting tankers to store the surplus supply and that has forced the price of U.S. oil into negative territory.

The severe drop on Monday was driven in part by a technicality of the global oil market. Oil is traded on its future price and May futures contracts are due to expire on Tuesday. Traders were keen to offload those holdings to avoid having to take delivery of the oil and incur storage costs.

June prices for WTI were also down, but trading at above $20 per barrel. Meanwhile, Brent Crude, the benchmark used by Europe and the rest of the world, which is already trading based on June contracts – was also weaker, down 8.9% at less than $26 a barrel.

OGUK, the business lobby for the UK’s offshore oil and gas sector, said the negative price of U.S. oil would affect firms operating in the North Sea.

The oil industry has been struggling with both tumbling demand and in-fighting among producers about reducing output.

Trump has said the government will buy oil for the country’s national reserve.

Oil rebounds in Asian trading

A Bloomberg report said:

Oil rebounded in Asian trading.

Futures in New York traded at around $1 a barrel after sinking to as low as minus $40.32 during Monday’s jaw-dropping collapse. The June contract, however, which had trading volumes more than 60 times higher, rose above $21. The spread between the two reflects the growing fear that those who take physical delivery of crude in the near future may not find any outlet or storage for those barrels as refineries curb operations.

Crude explorers shut down 13% of the American drilling fleet last week. While production cuts in the country are gaining pace, it is not happening quickly enough to avoid storage filling to maximum levels, said Paul Horsnell, head of commodities at Standard Chartered Plc.

In Asia, bankers are increasingly reluctant to give commodity traders the credit to survive as lenders grow ever more fearful about the risk of a catastrophic default.

Fund Inflow

Despite the weakness in headline prices, retail investors are continuing to plow money back into oil futures. The U.S. Oil Fund ETF saw a record $552 million come in on Friday, taking total inflows last week to $1.6 billion.

The price collapse is reverberating across the oil industry. Crude explorers shut down 13% of the American drilling fleet last week.

Goldman sees oil volatility before ‘violent rebalancing’

The oil market is set to be forced into a “violent rebalancing” over the coming weeks, according to Goldman Sachs Group Inc.

Price volatility will remain exceptionally high in the coming weeks, Goldman said in a note.

“With ultimately a finite amount of storage left to fill, production will soon need to fall sizeably to bring the market into balance, finally setting the stage for higher prices” once demand recovers, analysts including Damien Courvalin wrote in the note date April 20. “This inflection will play out in a matter of weeks, not months, with the market likely forced to balance before June.”

India stocks fall with Asian markets as growth worries intensify

A Bloomberg report said:

India’s benchmark stock gauge fell, tracking peers in Asia, as a plunge in oil prices heightened investor concerns about domestic growth.

The S&P BSE Sensex Index fell 2.8% to 30,774.23 as of 9:59 a.m. in Mumbai, and the NSE Nifty 50 Index declined by 2.7%. Asia’s third-largest economy is near a standstill amid a prolonged lockdown to prevent the spread of the coronavirus.

While India is a net importer of crude, a collapse in oil futures on Monday amid stagnant global demand exacerbated economic growth fears.

All major equity markets in Asia declined Tuesday, with the regional MSCI Asia Pacific Index dropping 1.9%.

India’s government and central bank are trying to cushion the economic effect of virus-enforced closures with fiscal and monetary policy measures. Some makers of information-technology hardware in India, farmers and industries in rural areas resumed operations from Monday even as the lockdown was extended until May 3.

“Efforts to ramp up the economy once the lockdown has been lifted may take a toll as the lack of employees as well as demand may strike down hard on industrial activity,” analysts at Motilal Oswal Financial Services Ltd. wrote in a note to clients.

With the earnings season underway, Infosys Ltd. on Monday refrained from projecting full-year revenue for the first time in years, joining a growing list of businesses around the world struggling to assess the fallout of the COVID-19. So far, four Nifty 50 members have reported quarterly results.

A hunt for any storage space turns urgent as oil glut grows

A Reuters report said:

With oil depots that normally store crude oil onshore filling to the brim and supertankers mostly taken, energy companies are desperate for more space. The alternative is to pay buyers to take their U.S. crude after futures plummeted to a negative $37 a barrel on Monday.

A topsy-turvy market that has oil prices for October delivery at $31 a barrel has oil firms anxious to sock away millions of barrels now to sell at a profit later.

While the government estimated there is available space, traders said Monday’s market drop indicated any unfilled tanks are under lease, and not available to new renters.

“The industry is really scrambling to source viable storage options,” said Stuart Porter, a manager at Adler Tank Rentals in Texas, which has shale companies lining up to potentially lease dozens of its 500-barrel steel frac tanks. The tanks can be lined up like dominos and filled at the well site by producers without a home for their oil. Converge Midstream LLC with millions of barrels of storage available in underground salt caverns outside Houston has gone from few takers to requiring one- to two-year contracts.

“Quite honestly we were struggling for business. Now that the market has changed, everyone is our friend,” said Dana Grams, chief executive of Converge Midstream.

The hunt for storage points to the magnitude of the collapse in demand for U.S. shale and the huge volume of unsold oil to refiners who are cutting purchases.

In addition to the onshore glut, there are about 160 million barrels of oil sitting on tankers waiting for buyers. At least six crude tankers carrying 2 million barrels apiece are en route to the U.S. from Saudi Arabia, adding to the alarm at the U.S. Gulf Coast.

It is not just crude looking for a place to go. State lockdowns have decimated demand for motor fuel. U.S. gasoline demand fell 32% earlier this month compared with the same time a year ago, the EIA said.

That glut is creating opportunities for some.

At Caliche Development Partners, which stores natural gas liquids in underground caverns near Houston, CEO Dave Marchese may shift his plans and open a newly completed 3-million-barrel underground salt-cavern for crude oil or gasoline.

“Gasoline has a pretty large contango right now,” he said, referring to prices five or more months ahead that are higher than current levels. But both fuels would require new pumps in its salt cavern, Marchese said, and he wants buyers to pay up for any upgrades.

Shale producer Teal Natural Resources had one of its three crude buyers cancel a purchase agreement last month, sending it shopping for frac tanks. They are not cheap, Teal CEO John Roby learned after scouring the market.

Storing a month’s worth of output would cost Teal about $20 a day per tank, or about $300,000 a month. At those rates, Teal would rather shut in wells, he said.

Shutting off wells is not for everyone, though, because it can reduce future oil recovery, and may put a producer in breach of their lease contracts.

Rentals for frac tanks have jumped from about $15 a day previously, a Texas oil marketer said.

Another oil producer, Texland Petroleum aims to sell immediately whatever crude it can this month, said its President Jim Wilkes. He is considering adding frac tanks to avoid having to pay to have his oil carried away in May.

Joshua Wade, an oil marketer in Oklahoma, is in talks to reserve about 100,000 barrels of storage for May using a combination of frac tanks, on-system pipeline storage and smaller tanks that have been dormant on pipelines.

But time is running out and costs are rising quickly.

“A lot of people have been calling me now and saying ‘I wanna go out and buy 100,000 barrels in May and put them in a frac tank,’” said Wade. “I tell them the party started about a month ago and it’s now almost over.”