This analysis provides a reassessment of dollar hegemony and power relations in the international monetary system.

Summary

Despite renewed predictions that dollar hegemony has reached its peak, the greenback continues to dominate global trade, finance and the reserve portfolios of central bankers around the world. But can high inflation, geopolitical tensions and the sanctions levied on Russia by the US and its allies dent its global dominance? Focusing on the impact of the COVID-19 pandemic, the war in Ukraine and the sanctions on Russia, and the ‘steep hike’ of interest rates by the Federal Reserve, this paper reassesses power relations in the international monetary system and analyses the state of dollar hegemony. It finds that, although the US dollar still reigns supreme, there are certain undercurrents that indicate the slow erosion of its global dominance and the gradual shift towards a multipolar currency order. To prevent, or at least slow down, the pace of further fragmentation, the West ought to re-evaluate the use of financial sanctions as a foreign policy tool and offer the Global South more voice in international monetary relations.

Analysis

(1) Introduction

More than a decade after the Global Financial Crisis (GFC), it is a good moment to reassess power relations in the international monetary system and analyse the state of US dollar hegemony. In the aftermath of the great recession, there was a certain consensus that it had reached its peak. For the first time, Chinese policymakers were openly calling for moving away from the greenback and starting in earnest to promote the renminbi’s (RMB) internationalisation. At the same time, the then-fashionable BRICS (Brazil, Russia, India, China and South Africa), which had weathered the crisis relatively well, also began having regular summits to promote the use of their domestic currencies. And even European leaders like Nicolas Sarkozy took advantage of France’s G20 presidency in 2011 to discuss how to reduce the world’s dollar dependence.

Since then, many important geopolitical events have happened. In 2012 the European debt crisis almost ended in Grexit, although the euro finally survived, and the eurozone, thanks to a series of ambitious reforms, became structurally more resilient. In 2016 Trump came to powerand pulled out of the Iran deal, pushing the Europeans to find alternative ways to conduct trade and settle energy imports (especially gas) without relying on the dollar. Then, in 2020, came the pandemic, again massive quantitative easing, and in 2022 the war in Ukraine with the consequent freezing of Russian assets in western countries, and in the same year a ‘steep’ hike of interest rates by the Federal Reserve (Fed) to fight their effects. The question, however, is whether these shocks have transformed the international monetary system in a substantial manner.

On the one hand, some argue that these episodes have only reinforced the centrality of the dollar. The greenback is still, by far, the global currency of choice, as individuals, corporations and monetary authorities continue to rely heavily on the dollar as a medium of exchange, a unit of account and a store of value. Moreover, the Fed remains the de facto central bank of the world, as evidenced by the enormous liquidity that it provided through its currency swap lines to both developed and developing countries during the COVID-19 lockdowns, as well as the dollar shock unleashed by its rising rate policy in Europe and beyond.

However, it is also true that the Trump years, which marked the start of a trade and tech warbetween the US and China, and the recent sanctions applied on Russia, have accelerated the desire of at least these two powers, but perhaps also of India, Brazil and the Gulf States, to de-dollarise even further and quicker. High inflation and the rise of alternative payment systems, such as the Chinese Cross-Border Interbank Payments System (CIPS), can also chip away at the dollar’s dominance. The recently re-elected President of Brazil, Lula da Silva, summed up well the increasing sentiment (and frustration) in the Global South by stating: ‘Every night I ask myself why all countries have to base their trade on the dollar… why can’t we do trade on our own currencies?’.[1]

So, although the US dollar still reigns supreme, is it possible that we are witnessing a slow but structural shift towards a multipolar monetary system? We find that, despite a prolonged fall in dollar reserves, the greenback’s standing across the other functions of money remains high. However, the increased reliance on financial sanctions as a foreign policy tool may discourage its international use by countries who fear falling from America’s grace, particularly in the Global South. Additionally, the slow but steady rise of alternative financial infrastructures could eventually push countries to seek different vehicle currencies, including their own. The efforts by China, in particular, to offer alternatives to dollar hegemony deserve close attention.

(2) The use of the dollar, the euro and the RMB

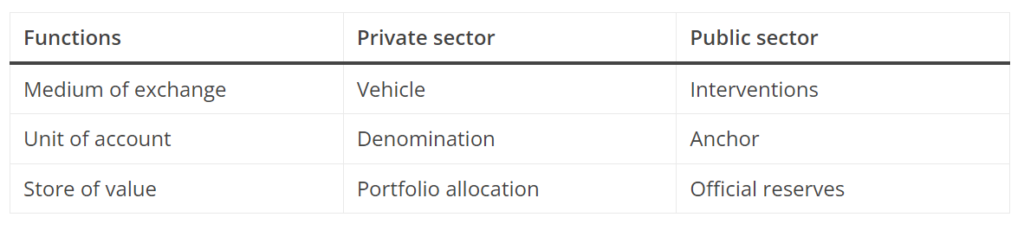

An international currency is any money that is used outside of its issuing state to fulfil three basic functions:

Figure 1. The functions of international currencies

According to Paul. R. Krugman (1984), ‘The international role of the dollar: theory and prospect’, in Richard C. Marston & John F. Bilson (Eds.), Exchange Rate Theory and Practice, University of Chicago Press. Source: the authors.

The US dollar remains the most widely used international currency across these three roles, and that has not changed much in almost a century. In fact, the greenback has long played an outsized role in global markets, far outstripping the US’s share in global trade, international bond issuance, and cross-border borrowing and lending. However, looking closely, there are signs of a gradual erosion in the dollar’s hegemony.

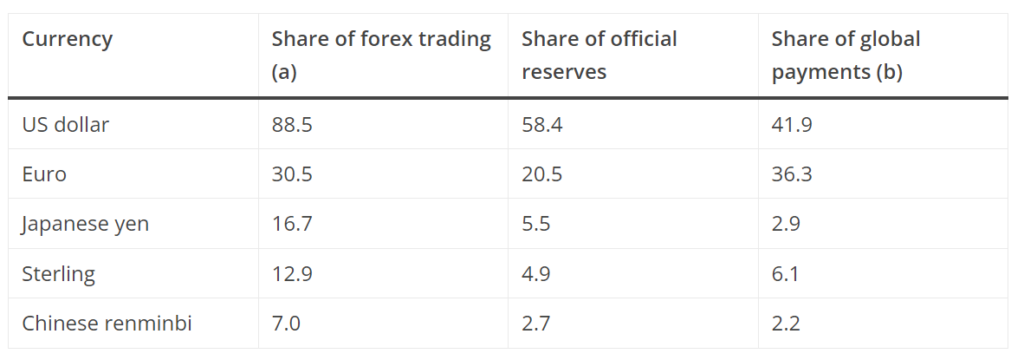

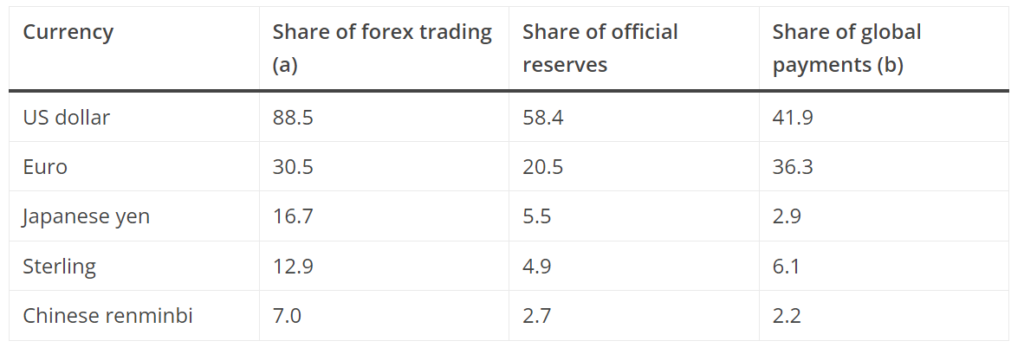

Indeed, in many ways, the greenback is still king. For example, as a vehicle currency, the US dollar completely dominates FX markets, accounting for 88% of all trade in 2022.[2] Similarly, it has been the world’s leading invoicing currency over the past two decades, denominating 96% of trade in the Americas, 74% in Asia Pacific and 79% in the rest of the world; the only exception is Europe, where the euro dominates.[3]

Nonetheless, whereas the role of the US dollar across the first two dimensions has remained broadly stable over the years, its share in official reserves has seen a prolonged decline since the turn of the century, dropping from 71% in 1999 to 58% in 2022. Some see today’s surging gold prices and falling dollar reserves as clear evidence of a future shift towards a multipolar currency order. But although it may still be early to tell, the reality is that we are witnessing a sustained effort by certain countries –particularly in the Global South– to reduce their dollar dependence.

(2.1) THE EURO

Meanwhile, the euro remains the second most important currency in the international monetary system, not fully threatening the dollar’s domination, but being far superior to Sterling, the Japanese yen and the Chinese RMB across the three functions of money.

But although its international standing has remained broadly stable in recent years –despite rising inflation pressures driven by COVID-19 and the war in Ukraine– its share across various indicators of international currency use remains close to historic lows. For instance, euro claims of official reserve assets stood at 20.5% at the end of 2022, far lower than the almost 30% it represented before the GFC. In FX markets the euro continues to be the second most actively traded currency, but its 30.5% turnover pales in comparison with the almost 90% of the US dollar. The one dimension where the euro is a fair contender against dollar dominance is in the share of global payments, where it accounts for 36.3% of SWIFT payment instructions versus the US dollar’s 41.9%.

All in all, a stronger international role of the euro will be one of the EU’s key pillar strategies to achieve greater economic and financial strategic autonomy in the future. For the first time, the EU is now issuing large quantities of debt to finance its pandemic recovery programme, which should help to deepen euro-denominated debt markets. But to subside its role as a junior partner of the US dollar, the EU will have to develop a deeper and more complete Economic and Monetary Union.

(2.2) THE CHINESE RMB

Lastly, the Chinese RMB remains a relatively small player in the international monetary system compared with the economic might of China, and this despite earlier (premature) predictions that it might dethrone the US dollar as the leading international currency. The incomplete openness of the capital account and the lack of full convertibility continue to weigh on the yuan’s global appeal. But geopolitical tensions, particularly China’s trade and tech disputes with the US, might also have hindered further progress.

Nonetheless, thanks to its strong economy and satellite offshore financial markets, the RMB moved quickly from not being used overseas at all to being among the top ten international currencies. Its international use peaked in 2015, when the IMF decided to include it in its special drawing rights (SDR) basket of currencies. However, since then the RMB’s internationalisation has somewhat plateaued despite Beijing’s active efforts.

For example, its share of official foreign reserves has increased in recent years, but remains modest compared with other major currencies, at around 2.7% last year. In terms of cross-border payments, SWIFT data point to a pickup of activity to over 2% in 2022, but this is still only enough to challenge the Japanese yen as the fourth top currency. And with 7% of global FX turnover, it is hard to say that the RMB is truly a global vehicle currency yet.

But the RMB’s rise should not be shunned. Although it is still far from constituting an impending threat to the US dollar, some of its achievements would have been unthinkable only a decade ago. For instance, in 2023 the yuan overtook the dollar as the most-used currency in China’s cross-border transactions. This year, China also completed its first RMB-settled liquefied natural gas (LNG) trade with France. And although the RMB’s share of trade credit is a meagre 4.5%, the figure has more than doubled since the start of Russia’s invasion.

Figure 2. Currency internationalisation comparison, 2022 (%)

According to Paul. R. Krugman (1984), ‘The international role of the dollar: theory and prospect’, in Richard C. Marston & John F. Bilson (Eds.), Exchange Rate Theory and Practice, University of Chicago Press. Source: the authors.

The US dollar remains the most widely used international currency across these three roles, and that has not changed much in almost a century. In fact, the greenback has long played an outsized role in global markets, far outstripping the US’s share in global trade, international bond issuance, and cross-border borrowing and lending. However, looking closely, there are signs of a gradual erosion in the dollar’s hegemony.

Indeed, in many ways, the greenback is still king. For example, as a vehicle currency, the US dollar completely dominates FX markets, accounting for 88% of all trade in 2022.[2] Similarly, it has been the world’s leading invoicing currency over the past two decades, denominating 96% of trade in the Americas, 74% in Asia Pacific and 79% in the rest of the world; the only exception is Europe, where the euro dominates.[3]

Nonetheless, whereas the role of the US dollar across the first two dimensions has remained broadly stable over the years, its share in official reserves has seen a prolonged decline since the turn of the century, dropping from 71% in 1999 to 58% in 2022. Some see today’s surging gold prices and falling dollar reserves as clear evidence of a future shift towards a multipolar currency order. But although it may still be early to tell, the reality is that we are witnessing a sustained effort by certain countries –particularly in the Global South– to reduce their dollar dependence.

(2.1) THE EURO

Meanwhile, the euro remains the second most important currency in the international monetary system, not fully threatening the dollar’s domination, but being far superior to Sterling, the Japanese yen and the Chinese RMB across the three functions of money.

But although its international standing has remained broadly stable in recent years –despite rising inflation pressures driven by COVID-19 and the war in Ukraine– its share across various indicators of international currency use remains close to historic lows. For instance, euro claims of official reserve assets stood at 20.5% at the end of 2022, far lower than the almost 30% it represented before the GFC. In FX markets the euro continues to be the second most actively traded currency, but its 30.5% turnover pales in comparison with the almost 90% of the US dollar. The one dimension where the euro is a fair contender against dollar dominance is in the share of global payments, where it accounts for 36.3% of SWIFT payment instructions versus the US dollar’s 41.9%.

All in all, a stronger international role of the euro will be one of the EU’s key pillar strategies to achieve greater economic and financial strategic autonomy in the future. For the first time, the EU is now issuing large quantities of debt to finance its pandemic recovery programme, which should help to deepen euro-denominated debt markets. But to subside its role as a junior partner of the US dollar, the EU will have to develop a deeper and more complete Economic and Monetary Union.

(2.2) THE CHINESE RMB

Lastly, the Chinese RMB remains a relatively small player in the international monetary system compared with the economic might of China, and this despite earlier (premature) predictions that it might dethrone the US dollar as the leading international currency. The incomplete openness of the capital account and the lack of full convertibility continue to weigh on the yuan’s global appeal. But geopolitical tensions, particularly China’s trade and tech disputes with the US, might also have hindered further progress.

Nonetheless, thanks to its strong economy and satellite offshore financial markets, the RMB moved quickly from not being used overseas at all to being among the top ten international currencies. Its international use peaked in 2015, when the IMF decided to include it in its special drawing rights (SDR) basket of currencies. However, since then the RMB’s internationalisation has somewhat plateaued despite Beijing’s active efforts.

For example, its share of official foreign reserves has increased in recent years, but remains modest compared with other major currencies, at around 2.7% last year. In terms of cross-border payments, SWIFT data point to a pickup of activity to over 2% in 2022, but this is still only enough to challenge the Japanese yen as the fourth top currency. And with 7% of global FX turnover, it is hard to say that the RMB is truly a global vehicle currency yet.

But the RMB’s rise should not be shunned. Although it is still far from constituting an impending threat to the US dollar, some of its achievements would have been unthinkable only a decade ago. For instance, in 2023 the yuan overtook the dollar as the most-used currency in China’s cross-border transactions. This year, China also completed its first RMB-settled liquefied natural gas (LNG) trade with France. And although the RMB’s share of trade credit is a meagre 4.5%, the figure has more than doubled since the start of Russia’s invasion.

Figure 2. Currency internationalisation comparison, 2022 (%)

Notes: (a) as two currencies are involved in each transaction, the sum of shares in individual currencies will equal 200%; and (b) including intra-eurozone payments. Source: the authors, with data from BIS (2022), IMF (nd) and SWIFT (nd).

(3) The current state of the international payment infrastructure

In response to Russia’s unprovoked military aggression, the US and its allies imposed harsh financial sanctions to ban Russian banks from the SWIFT network, stop domestic institutions from doing business with blacklisted organisations and freeze the Central Bank’s assets held in the West. While the true effectiveness of these sanctions is still widely debated, the measures have renewed talks in Russia, as well as in other countries in the Global South, about the potential alternatives to the current international monetary system.

As Barry Eichengreen pointed out in 2022:

‘Specifically, countries are looking at China, which has large internationally active banks, has created its own clearinghouse for cross-border transactions and is embarked on a campaign to encourage broader international use of its currency, the renminbi.’

But how far has China gone in creating alternatives to SWIFT, Western clearinghouses and the dollar? And could it draw other countries towards this parallel international financial universe?

(3.1) THE US-LED INTERNATIONAL PAYMENTS SYSTEM: SWIFT & CHIPS

The first step is analysing the current state of the Western-led international payments infrastructure, represented by SWIFT and CHIPS.

SWIFT is a member-owned cooperative society that is primarily associated with its financial payments messaging system. Using standard codes and formats, SWIFT has dramatically reduced the costs of translation and identification, becoming the main messaging network through which international payments are initiated. Banks around the world send and receive these messages to debit or credit customers’ accounts, not just in dollars but also in other currencies.

Crucially, SWIFT is also a vehicle through which the US government monitors compliance with financial sanctions. SWIFT messages generate vast amounts of financial data, which the Treasury department can use to trace financial flows and combat illicit financing. Notably, the US is able to do this despite the fact that SWIFT is a private cooperative with headquarters in Brussels. US banks are only minority shareholders, but other banks, fearing secondary sanctions, have often sided with their US peers. On some occasions, Washington has even threatened to sanction SWIFT directly.

Banks that are banned from SWIFT must find other ways of communicating with foreign counterparts, but Russia and other countries in similar positions have alternatives at their disposal. They can use other Internet channels, the telephone, even the fax, and, looking forwards, blockchain. However, these alternatives also have their associated costs: they are slower, less secure and inefficient when it comes to ‘bespoke’ transactions that require time and effort to verify information.

The second important infrastructure that supports dollar dominance, and which is less known, is the US Clearing House Interbank Payments System, or CHIPS, which functions as an actual clearing mechanism for transferring large-value payments. Like SWIFT, it is also privately owned and a vital element of the US-led international payments system, settling US$1.8 trillion in domestic and international payments per day. It consists of more than 40 direct participants (both US banks and US branches of foreign banks), which clear payments among themselves and on behalf of other financial institutions. Together with Fedwire, the Fed’s real-time gross settlement system, they make up for the primary network for domestic and foreign large value transactions denominated in US dollars.

Importantly, because CHIPS moves money between accounts, not just messages, finding a way around Western clearinghouses may not be as easy as with SWIFT. And even if it was, targeted countries would still have to find another vehicle currency other than the dollar to settle their international transactions. Hence, relying on CHIPS for settling cross-border payments could spell risks for countries with a difficult relationship with the US, particularly considering the amount of international trade that is still denominated in dollars.

(3.2) CHINA’S ALTERNATIVE FINANCIAL INFRASTRUCTURE

Increasing the international use of one country’s currency poses several challenges, as evidenced by the case of China. The first is that other countries should be willing to accept payment in that currency. In other words, recipients should be confident that the currency will hold its future value but also have a present use for it, for example, to import merchandise or invest in financial assets. In this respect, the fact that RMB-denominated payments have stayed at around 2% of total cross-border interbank settlements for much of the last decade suggests that potential recipients still see little use for it.

The second is that it should be possible to trade the currency at a reasonable cost. The People’s Bank of China (PBOC) has sought to achieve this by signing a number of bilateral swap agreements with foreign central banks to provide liquidity for direct trades and so remove the need to purchase US dollars first. However, these swap lines have rarely been activated for trade-related purposes. Instead, they have mostly been used to provide emergency lending and refinance debt to partners in need. The problem is not so much that foreign partners do not have access to cheap RMBs, but that they prefer to use other currencies.

The third is that there should be a reliable mechanism for transferring payments between domestic and foreign entities, which is where a Chinese clearinghouse comes in. In 2015 the PBOC launched CIPS, a RMB-based interbank payment system to serve as an alternative to both SWIFT and Western clearinghouses. It is divided into direct participants (currently 77 –mainly Chinese banks’ overseas branches–), who maintain an account in the system, and indirect participants (1,283, three-fifths of them outside China), who deal with it via the former.

Yet, for the moment, it would be difficult to argue that CIPS constitutes a serious challenge to Western clearinghouses since CHIPS has 10 times as many participants and processes 40 times as many transactions. It is one thing to build the highways (infrastructure) through which traffic (credit) can flow, but there is no guarantee that other countries will want to use them. In its efforts to increase its international currency use, China has built many of these highways to encourage other countries to move away from the dollar, but structural issues, such as China’s relatively closed capital account –which keeps transaction costs high–, may be preventing widespread adoption.

However, transactions in the CIPS network are growing, and while Chinese banks still constitute the bulk of (particularly direct) participants, other countries could join in the future. It is likely that US allies would steer clear of CIPS in fear of triggering retaliation from Washington, but countries already targeted by US sanctions, at risk of facing future sanctions, or simply looking for a more direct way to trade with China, might not. Russia has started accepting RMB for its energy exports to China, presumably through CIPS, and could use those receipts to purchase merchandise from Chinese suppliers or stabilise the rouble exchange rate. In this respect, CIPS may already be undermining dollar hegemony by diluting the impact of Western sanctions and reducing their overall effectiveness.

Another monetary highway infrastructure that should be considered is the potential of a future Chinese central bank digital currency (CBDC). The PBOC has probably gone further than any other large-country central bank in its efforts to launch a fully functioning CBDC and has achieved great progress in both retail and wholesale applications.[4] The eCNY (digital RMB) is still a working prototype that, like other CBDCs, has struggled to encourage widespread adoption. But once fully developed, it could eliminate the need to send payment instructions between banks or for settling transactions through a Western clearinghouse. One project in particular, the multi-CBDC mBridge initiative, developed in conjunction with Thailand and the United Arab Emirates, has recently shown promising results for cross-border digital payments and could help China promote its currency’s international use.

More broadly, countries could also use other blockchain channels to undermine the dollar’s dominance and circumvent Western sanctions. In fact, cryptocurrencies have been utilised by countries like Iran and North Korea to pay for imports and make up for lost revenues, so it could also be leveraged by Russia, albeit in more limited ways. However, these channels have not been tested at large scale, so it is possible that these concerns may be overstated.

(4) Power relations in monetary affairs

After mapping international currency use and the global payments infrastructure, we must ponder the economic and political implications of all of this for the US, its allies, its geopolitical rivals, and for global economics and politics at large. Specifically, we want to know whether the COVID-19 pandemic, the war in Ukraine, and the ‘steep hike’ of the Fed have accelerated the completion of alternative financial arrangements and the transition to a multipolar currency order. Or, to the contrary, whether these episodes are a simple reflection of the dollar’s extraordinary dominance in international monetary and financial affairs.

Those in the second camp argue that the dollar still reigns supreme, not only because of US geopolitical power, but also because it is a commercial and financial network, which is ubiquitous and quite flexible in adapting to new circumstances.[5] There is certainly an asymmetry between financial relations, heavily dominated by the West and particularly the US, and trade, investment and economic relations at large, which are increasingly multipolar. But all three major events over the past five years have shown the extraordinary power of the dollar and the centrality of the Fed in financial and monetary relations.

However, dollar dominance is not absolute and indefinite. There are certain undercurrents that show that while the eurozone, and by extension the euro, have become more subordinated to the US dollar with the War in Ukraine, other powers may be looking to move away from the greenback, despite the structural hurdles that this endeavour entails.

(4.1) SANCTIONS OVERREACH

The first way to look at this issue is through a static and macro analysis of the international monetary system, focusing on the current effects of the financial sanctions on Russia for broader monetary relations.

Over the years, several experts have argued that conditioning the use of the dollar on adherence to US foreign policy would risk antagonising foreign governments and encourage the migration to other financial systems. But despite these warnings, financial sanctions became one of the main foreign policy measures in the Western toolkit, as the US and its allies had been willing to accept the direct consequences of their actions. For example, when the US levied sanctions against Russia, Venezuela and Turkey in the 2010s, these measures increased perceptions of political risk among their leaders and set off a variety of efforts to reduce dependence on the greenback.[6] However, these were generally seen as isolated cases which, if anything, would mainly discourage other countries from ‘misbehaving’.

But now that 30% of all countries are facing sanctions from the West (up from 10% in the 1990s), the indirect effects of these measures have become visible. Indeed, the Global South’s response to the Russian invasion of Ukraine seems to support this ‘sanctions overreach’ theory. First came Putin, who called on its partners in Asia, Africa and Latin America to adopt the RMB for cross-border payments. That a Russian leader calls for the use of the Chinese currency in international trade is a clear symptom of how (monetary) power relations are shifting. Then came Lula, wondering ‘why every country needs to trade in the dollar’ and ‘who decided it was the dollar after the disappearance of the gold standard?’. The BRICS have long aspired to de-dollarise, but this trend is spreading. Lately, ASEAN finance ministers and central bankers are now also considering dropping foreign currencies in exchange for local ones.

But these de-dollarisation campaigns have not yet substantially dented the greenback’s global dominance. The attempts to diversify reserve assets away from the dollar appear modestly successful, but sustained efforts to reduce reliance on the US dollar as an international medium of exchange have achieved a lot less. As much as certain governments oppose US foreign policy, they have found it difficult to abandon the greenback completely because the benefits of dollar-use remain high. The ubiquity of the dollar makes it a cheap and convenient vehicle currency, and the fact that its centralised network is so established makes it hard for outsiders to challenge. Hence, the full implications of the Western sanctions against Russia remain uncertain.

Certainly, economic considerations still matter. Russia and other countries may want to move away from the dollar, but alternatives still lack the financial attributes to appeal to global investors. Furthermore, Russia’s unprovoked military aggression also serves as a reminder of the relevance of geopolitics for international currency status. Indeed, the risk of an escalating conflict over Taiwan, for example, could hinder China’s future efforts to increase its international currency use, since that could also trigger a heavy sanctions regime from the West.

Ultimately, ideas, interests and institutions play an important role. In the last two centuries the leading international currencies have been issued by countries with sound democratic institutions, durable international alliances and solid legal systems that protect property rights. Countries may opt to hold the greenback not only because of its economic benefits, but because they support the liberal, rules-based international order that it represents, suggesting that countries like China might have to undergo some degree of political reform before their currency can become a top contender (at least for international financial investors who operate mostly under liberal norms).

(4.2) ALTERNATIVE FINANCIAL AND MONETARY ARRANGEMENTS

The second way to see the threat to dollar dominance is through a dynamic and structural analysis of the international monetary system, focusing on the development of alternative financial arrangements such as the CIPS.

As mentioned, the sanctions levied on Russia have left the country looking for alternative ways to invoice exports and execute cross-border transactions. Seeing how costly this is proving for Moscow, other countries, worried about future conflicts with the West, have also started to look for options that might free them from SWIFT, CHIPS, and the dollar. Thus, in recent years, an increasing number of countries in the Global South have expressed desires to participate in other financial arrangements to diversify away from the greenback and increase trade and investment with partners without relying on it as a vehicle currency.

For the first set of countries, China is an obvious candidate due to its general opposition to US foreign policy. Russian officials, for example, estimate that China will likely remain neutral in the war in Ukraine, so doing international business through Chinese financial institutions is helping them circumvent US sanctions and weaken the West’s coalition. China already constitutes a major market for Russian energy exports, and the RMB can be used for purchases of merchandise and material, pay for infrastructure projects, and buy government bonds. In fact, this is already happening with the help of smaller, regional Chinese banks without much exposure to the global financial system, so other countries could see this as an insurance against future conflicts with the West.[7]

But for countries outside the scope of current or future Western sanctions, China may also be seen as a potential contender to develop a viable alternative to the US-led international monetary system because of its economic and financial weight. For one, it is the world’s largest exporter and second-largest importer by value. In recent years, China has also become the top trading partner to more than 120 countries, especially those in the Global South. And, according to UNCTAD, China is also the first country in terms of foreign direct investment outflows and second in terms of inflows. If foreign importers were increasingly encouraged to settle payments in RMB and borrow yuan-denominated loans, particularly those participating in the Belt and Road Initiative, CIPS and China’s swap lines could become an increasingly vital financial infrastructure for many countries.

However, many have pointed out that China’s structural limitations will probably constrain the widespread adoption of its currency in international markets and the participation of foreign entities in its alternative financial architecture. They argue that, despite Beijing’s active efforts to undermine dollar hegemony, the evidence indicates that these have not achieved much yet. For instance, the fact that the RMB’s share of FX reserves is a mere 2.7%, with just one country –Russia– holding nearly a third, shows that it cannot rival Western alternatives. Following the setting-up of the oil futures market in Shanghai in RMB, there has been a lot of talk about the possibility of the Gulf states starting to invoice their oil in yuan, although this is unlikely for now.[8] Similarly, seeing how China’s swap lines have rarely been activated for trade-related purposes, some suggest that they have been broadly ineffective at promoting trade settlement in their currency. And given that more than seven years after its launch, CIPS still accounts for a relatively small network of (mainly Chinese) banks, it is hard to argue that it constitutes a real threat to Western clearinghouses.

But this maximalist view is too quick to disregard the PBOC’s important milestones in its enduring campaign of currency internationalisation. The inclusion of the RMB in the IMF’s SDR basket of currencies in 2015, for example, represents an important recognition of the yuan as an international reserve currency. China’s swap lines have become a short-term liquidity backstop and debt restructuring tool for partner countries in financial need, and this has demonstrated the country’s increasing role as an international lender of last resort.[9] And although CIPS is far from rivalling Western clearinghouses, its development certainly constitutes a great achievement insofar as it proves China’s ability to build an advanced inter-bank payment system capable of processing large-value payments. Rather than comparing it with other major international currencies, it is China’s incremental progress in de-dollarisation that should be measured. Considering that the country has achieved all this (and perhaps even more than meets the eye because a lot of RMB use might go under the radar of international statistics) in barely a decade, it can only be wondered what might happen in the next.

Nonetheless, structurally speaking, the core of US monetary power, and by extension the lack of China’s capacity to challenge it, lies in its ability (and willingness) to run large balance of payment deficits to supply the world with its currency. The US remains the consumer of last resort of the world economy, with a current account deficit of US$943.8 billion (or 3.7% of GDP) in 2022, and the fact is that the world is ready to provide it with the necessary credit (and thus generate a large demand for dollars) to continue to perform this role –at least for now–. This would, of course, change if the political deadlock in the US Congress should prevent lifting the debt ceiling and the US were to enter into default.

Conclusions

What next?

To sum up, the dollar remains dominant, but there are many powers that want to move away from it. Nonetheless, the truth is that all the alternative arrangements are still much smaller in scale and scope than the dollar network. The BRICS called many times to de-dollarise, but the dollar remains the currency of choice for governments, firms and financial institutions around the world to conduct trade and investment. The RMB, the currency with most potential to rival the greenback, is still not very important in its international use and it could take a while before it reaches the dollar, or even the euro, as an international currency, if at all. So, as Susan Strange would put it, we are again discussing the persistent myth of lost US dollar hegemony.

However, China’s push for international currency use has been on cautious and focused bilateral uses, and in this area progress has been substantial. If the question is when will China’s alternative arrangements constitute an actual threat to US hegemony, then the answer is probably no less than a decade. But if the focus is on China’s effort to boost its currency’s international standing and reduce dollar dependence, then the picture looks different.

If a post-dollar multipolar monetary system were to arrive, what would it look like? There is a long-standing debate in international monetary theory between proponents of hegemonic stability a la Kindleberger and those who support a multipolar currency world, chief among them Eichengreen, but even in the latter scenario, the loss of dollar hegemony will probably not spell the end of US might. As the leader of the largest security network in the world, the country could benefit from a shift towards great power rivalry, despite the dollar facing greater competition from the currencies of geopolitical rivals.

However, the loss of power might still cause some pain. Martin Wolf from the Financial Timesand others have warned of the risks of a post-dollar world and a bipolar international monetary system, with the US and China at opposite ends. If this latter scenario were to come true, then the US would suffer a severe decline in its ability to project global economic influence, with profound implications domestically and for the international order.

Instead, the US might decide to rethink its approach to financial sanctions and help protect the dollar’s international status by designing them in a way that prevents the further erosion of the unipolar currency order. In particular, the West should avoid forcing other states to choose sides and instead build voluntary sanctions coalitions. The use of sanctions should also be reserved for extreme cases that constitute a clear threat to world order instead of conditioning the use of the dollar and its financial system on adherence to US foreign policy. Finally, the international financial and monetary institutions need to be reformed to accommodate a bigger role for the Global South.

All in all, then, the international monetary system reflects the power configuration in international relations. The US is still dominant but in relative decline, while the war in Ukraine has shown the dependence of the Eurozone, the issuer of the second most significant international currency, on US military guarantees. In this regard, the West, including its Asian allies such as Japan and South Korea, appears relatively united, certainly more than during the Trump years. But at the same it is more detached from the Global South, which has not followed the sanctions against Russia and is increasingly willing to find alternatives to the US dollar. This is, indeed, a clear signal that while US (dollar) hegemony is still with us, it is also progressively more contested.